Follow Us :

Construction & Engineering Insurance Market Report: Size, Share, Trends, and Forecast (2024-2033) – By Type and Application

- Report ID: STAR4625

- Industry: Finance & Banking

- Published Date: 19-06-2025

- NUMBER OF PAGES: 211

-

FORMAT:

Construction & Engineering Insurance Market Research: 2033

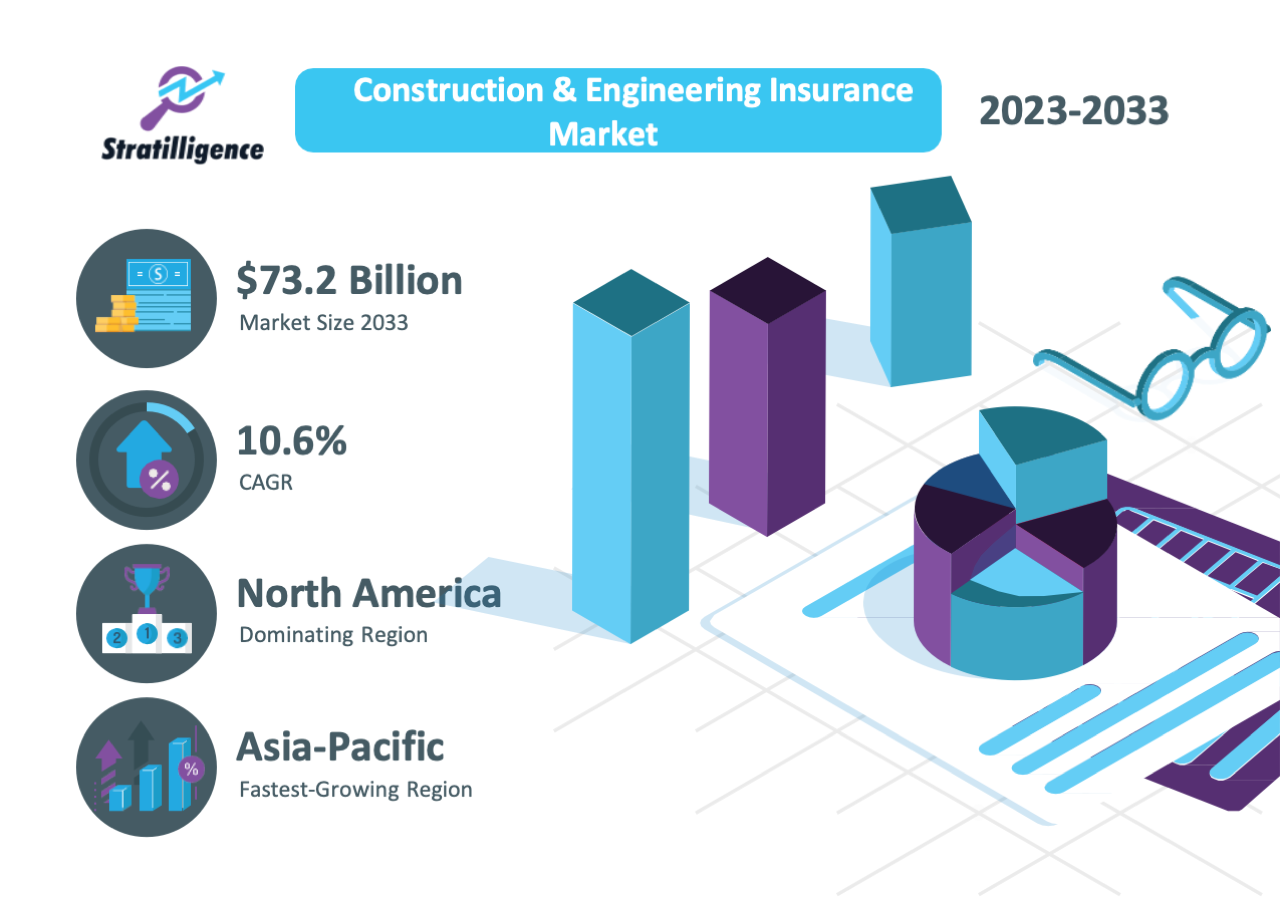

The global construction & engineering insurance market size was valued at $26.2 billion in 2023 and is projected to reach $73.2 billion by 2033, growing at a CAGR of 10.6% from 2024 to 2033. Construction & engineering insurance is a specialized type of insurance designed to provide financial protection and risk coverage for construction & engineering projects. It safeguards stakeholders, including contractors, project owners, engineers, and financiers, against potential losses and liabilities arising from unpredictable events during the lifecycle of a project.

Construction engineering generally involves contractors, subcontractors, architects, engineers, and owners. The marketplace offers products such as third-party insurance and workers’ compensation insurance to compensate these participants for legal claims or damages due to negligence, errors occurring systematically, or as a result of an on-site accident. This coverage ensures that businesses can continue unhindered by financial and legal challenges.

The primary beneficiaries of these types of insurance are contractors, architects, engineers, contractor owners, developers, and government agencies, public organizations

Construction professionals are primarily builders and vendors of construction technology insurance. They rely on policies such as contractor all risk (CAR) insurance and builder’s risk insurance to protect their projects against potential risks such as property damage, equipment failure, and on-site accidents. Business owners and contractors responsible for financing and managing construction projects are the main buyers in this market.

Insurance is required to mitigate the risks of delays, legal liabilities, and construction defects. Policies such as delay in start-up (DSU) insurance are particularly valuable to these stakeholders, as they protect against financial losses that could jeopardize business viability.

Engineers and architects, and other professionals often purchase this insurance to protect against claims resulting from design defects, negligence, or omissions. Normal compensation is especially important in complex construction projects, as errors in planning or design can have significant financial and reputational costs.

The construction & engineering insurance market is growing rapidly, driven by the global push for infrastructure development. It is a major driver of the market. Government and private companies invest heavily in major projects such as roads, bridges, airports, and railways. These expensive projects carry significant risks, including property damage, delays, and equipment failures, leading to a demand for comprehensive insurance solutions that offer maximum financial protection.

Rapid urbanization and population growth, especially in emerging economies, are increasing the demand for residential and commercial buildings. This growing construction industry requires insurance coverage for a variety of risks, from on-site accidents to construction defects. Insurance policies designed for these industries are an important resource for contractors and investors.

Many governments have introduced mandatory insurance requirements for the construction industry, such as contractor all risk (CAR) insurance or builder’s risk insurance. The aim of these regulations is to protect stakeholders from financial and legal risks and to ensure that the business is compliant and stable. In the UAE and France, for example, ten-year insurance is a legal obligation for major construction projects, further boosting market growth.

As the construction industry becomes more complex, stakeholders place more emphasis on risk management. Insurance is seen as a practical tool for dealing with potential problems such as natural disasters, cyberattacks on connected systems, supply chain disruptions, etc. This growing awareness is driving the demand for robust and scalable insurance solutions.

Key Market Drivers and Growth Factors in the Construction & Engineering Insurance Market

The growth of the construction & engineering insurance market is pushed by several key factors. The adoption of technologies such as building information modelling (BIM), drones, and IoT devices introduces new risks such as cybersecurity threats and data breaches. The construction & engineering insurance market is adapting to meet these emerging challenges, ensuring that businesses remain secure in an increasingly digital environment. These changes expand the construction & engineering insurance market, attracting new customers.

Also, emerging countries in Asia Pacific, Latin America, and Africa are experiencing rapid industrialization and urbanization, leading to increased construction activity. These regions present significant growth opportunities for construction & engineering insurance providers, as they need to cover infrastructure, which will be jobs, residential, and renewable energy installations, driving the cost market growth in these areas.

Coverage of the report

| Scope | Details |

|---|---|

| Market Size Estimation | Quantitative Insights: Market size and projections from 2019 to 2033, Market Size Units: USD Billion |

| Market Dynamics | Analysis of drivers, restraints, and trends shaping the market |

| Industry Analysis | Value chain analysis, Profit margin analysis, and Industry Overview |

| Segmentation | By Type (Construction Project All Risks Insurance, and Installation Project All Risks Insurance), By Application (Construction Enterprises, Real Estate Enterprises, Production and Processing Enterprises, Energy Production and Supply Enterprises, Others) |

| Region Insights | Detailed analysis for North America, Europe, Asia-Pacific, Latin America, and MEA with key countries in each region |

| Competitive Analysis | Company profiles, Ranking/Market share analysis, Competitive structure, Product differentiation |

| Customer Landscape Analysis | In-depth understanding of the customer industry, preferences, and buying patterns |

| Supplier Analysis | Comprehensive analysis of suppliers |

Key Benefits for Stakeholders

This comprehensive report provides stakeholders with in-depth qualitative and quantitative analyses, focusing on the global construction & engineering insurance industry from 2023 to 2033.

Key benefits include:

- Insightful construction & engineering insurance market forecast: The report offers detailed projections, covering various segments, current trends, and market dynamics.

- Competitive Analysis with Porter’s Five Forces: A thorough examination of the bargaining power of buyers and suppliers, the threat of new entrants, competitive rivalry, and substitute products.

- Comprehensive Market Overview: Gain access to crucial information about key market drivers, restraints, and opportunities.

- Regional and Country-Level Mapping: The report maps out major regions and countries based on their revenue contribution to the global market.

- Market Player Positioning: The competitive landscape analysis provides a clear understanding of the current market positioning of key players.

Regulatory Mandates in the Construction & Engineering Insurance Market

Governments around the world are increasingly mandating certain types of insurance for the construction & engineering sectors to ensure financial efficiency, risk reduction, and compliance with safety standards. This regulation aims to protect contractors to owners, to the general public. For example, many states require contractors to have all-risk (CAR) insurance, which covers property damage, construction site accidents, and delays.

By 2026, several Asian countries, including Thailand and Vietnam, will be introducing such mandates for large-scale infrastructure projects, making insurance an integral part of project planning and management. For instance, in France, ten-year insurance has been mandatory for all construction projects since 1978. In addition, in the UAE, owners reinforced this requirement in 2023 as part of new legislation, which ensures long-term protection of the building. These regulations have increased the demand for specialized insurance products, ensuring that construction projects are adequately protected against damage to buildings and third-party coverage.

Challenges and Restraints in the Construction & Engineering Insurance Market

One of the major challenges facing the construction & engineering insurance market is rising premiums. Insurers increased premiums for various insurance products as claims for natural disasters, cyber-attacks, and accidents increased in 2023 and 2024. This placed a financial burden on employees, contractors, and them operating on the project, especially in areas prone to frequent natural disasters such as cyclones, floods, and earthquakes. Besides this factor, the cost of construction materials is rising, which has also contributed to the increase in insurance costs, which in turn affects the overall cost structure of construction projects.

As the construction & engineering industry evolves with new technologies, it is difficult to quantify and insure emerging risks. The integration of digital tools such as building information modelling (BIM), drones, and IoT devices creates cybersecurity vulnerabilities that are not adequately addressed by traditional insurance systems. The systems are not as up-to-date as they could be, reflecting technological advances in the industry. This limitation of coverage is a severe restriction on market growth.

Construction & Engineering Insurance Market Segmentation

The construction & engineering insurance market is bifurcated based on type and application. By type, the market is categorized into construction project all risks insurance and installation project all risks insurance. In 2023, the Construction Project All Risks (CPAR) Insurance segment is expected to be the largest within the construction & engineering insurance market. CPAR insurance provides coverage for property damage, third-party claims, and risks associated with accidents during the construction period. It is widely adopted in a variety of construction projects, from residential to large-scale infrastructure projects.

By application, it is segmented as construction enterprises, real estate enterprises, production and processing enterprises, energy production and supply enterprises, and others. In 2023, construction project all risks (CPAR) Insurance is set to remain the largest segment due to its widespread use across various types of construction projects. The expansion of complex installations in areas such as renewable energy, advanced industrial performance, and advanced infrastructure is expected to drive the market growth.

Regional Analysis of the Global Construction & Engineering Insurance Market

Region-wise, the construction & engineering insurance market analysis is conducted across North America (the US and Canada), Europe (UK, France, Germany, Italy, and Rest of Europe), Asia-Pacific (China, Japan, India, South Korea, and Rest of Asia-Pacific), and Latin America (Brazil, Mexico, Argentina, and Rest of Latin America), and MEA (Saudi Arabia, UAE, Kenya, South Africa, and Rest of Middle East & Africa).

Competition Analysis

The major players profiled in the construction & engineering insurance market report having significant market share included are State Farm Mutual Automobile Insurance Company Prudential Financial Inc., Aetna Inc., RSA, Cardinal Health, Swiss Re, MetLife Services, Ping An Insurance (Group) Company of China Ltd, Allstate Insurance Company, and Allianz.

Key Developments/ Strategies in Construction & Engineering Insurance Market

Major companies in the construction & engineering insurance market outlook have adopted product launch, partnership, business expansion, and acquisition as their key developmental strategies to offer better products and services to customers in the market, which is contributing to the construction & engineering insurance market growth.

- In 2024, Ryan Specialty agreed to acquire US Assure Insurance Services, a US-based specialized builder’s risk insurance firm, for up to $1.48 billion. This acquisition enhances Ryan Specialty’s capabilities in the builder’s risk insurance sector, serving the small to middle market in the US

- In 2024, Zurich and Aon introduced a new insurance scheme to support the development of hydrogen production, a key component in transitioning to clean energy. The platform, involving multiple insurers led by Zurich, aims to underwrite smaller projects with capital expenditures up to $250 million. The coverage spans from construction to operational risks, addressing concerns about the insurance industry’s capacity to support green energy projects.

To explore the complete range of topics and critical insights our report offers, including comprehensive chapter names and pivotal sections, we invite you to submit a request for a detailed sample. Your inquiry will help gain an in-depth perspective on the report’s valuable content.

Chapter 1: Executive Summary

-

- Overview of the report

- Key findings and insights

- Market Entry Strategy (Add-on)

- Strategic Recommendation

Chapter 2: Introduction

Chapter 3: Market Overview

Chapter 4: Construction & Engineering Insurance Market, by Type

Chapter 6: Construction & Engineering Insurance Market, by Application

Chapter 7: Construction & Engineering Insurance Market, by Region

Chapter 8: Construction & Engineering Insurance Market, by Country

Chapter 9: Customer Industry Analysis (Add-on)

-

- Price Sensitivity Analysis

- Purchase Criteria Analysis

- XX

- XX

- XX

- XX

- XX

- XX

- XX

- XX

- XX

Chapter 10: Supplier Analysis (Add-on)

-

- Industry Structure Analysis

- Switching Cost Analysis

- XX

- XX

- XX

- XX

- XX

Chapter 11: Competitive Landscape

Chapter 12: Company Profiles